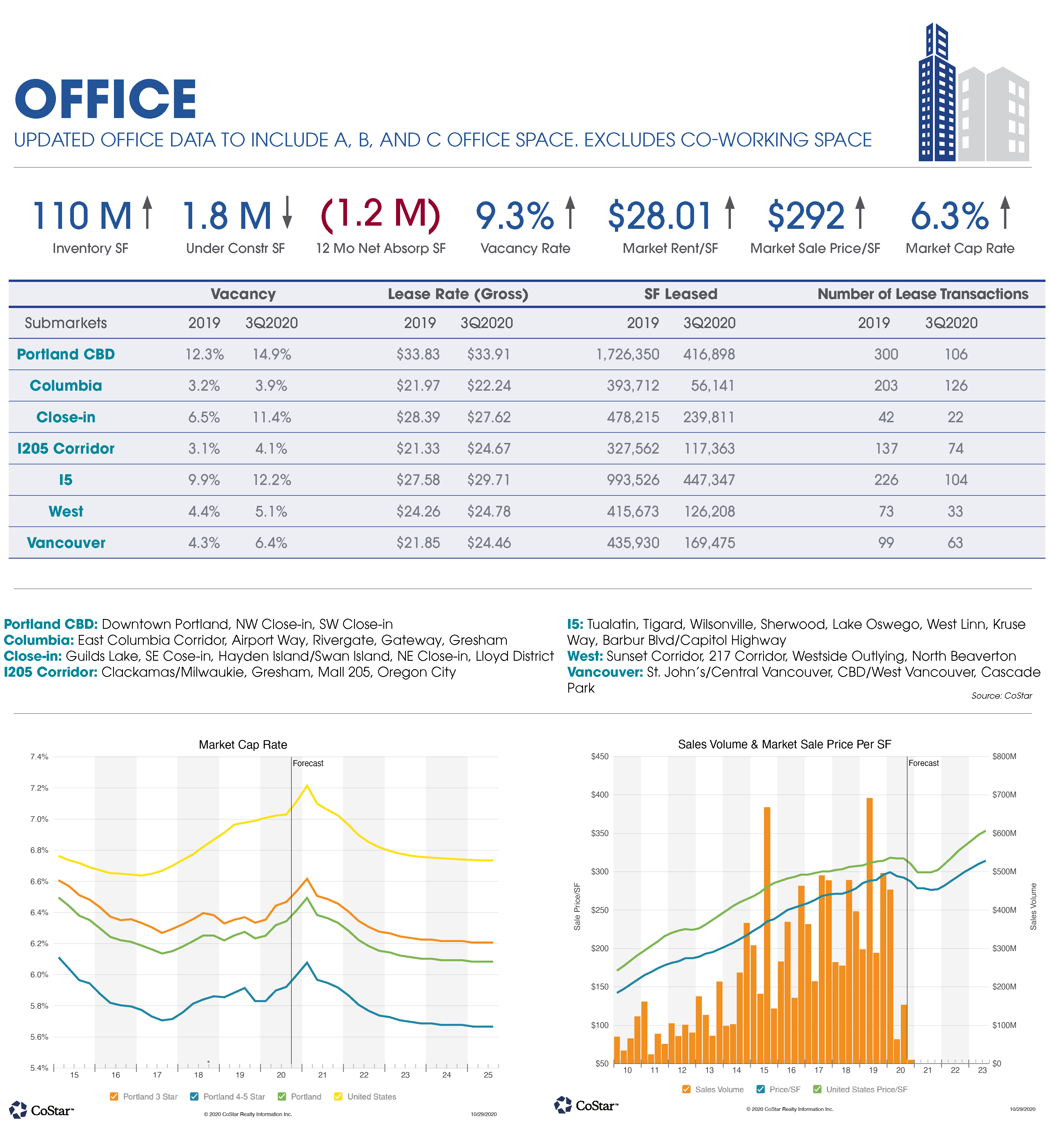

3Q 2020, continues the year’s overall trends in the office world. Vacancy and sublease rates continue to rise, while demand for space has shifted away from the long sought-after CBD into the Westside suburban markets. Vacancy in the total Portland market has reached 9.3% and is projected to reach 11.3% before falling again near 4Q 2021. Sublease vacancies also continue to emerge, with large tenants like Vacasa, Digital Trends, Sulzer Pumps, and Daimler Trucks North America re-evaluating their needs for space in a dynamic workforce environment. The increased vacancy and sublease vacancy combined with a smaller tenant pool should foster extreme competition for new leases, and will keep buoy vacancy in the short term. Over 1M SF of sublease space is now available in the market. The evolving questions surrounding workstyle and safety during the pandemic are primarily to blame for the trends, and the civil unrest – in the downtown areas primarily – has only exaggerated them. The suburbs have grown in popularity because of lower lease rates, abundant parking, and favorable taxation relative to downtown locations. Lease rates are expected to remain fairly constant in the suburban markets in the near term, while the CBD’s average rents are expected to decline by roughly 6% into mid-2021.

Sale transactions in the office world were resuscitated somewhat in Q3 after low transaction volumes in Q2, where the market experienced $62.5M in total sale volume, representing the market’s lowest sale volume in a quarter since 4Q 2011. Investor appetite showed growth, underscored by the $130M sale of Nimbus Corporate Center between Shorenstein (seller) and DRA Advisors LLC and Prescott Partners (buyers). Sale prices in the Portland market have leveled off since the beginning of 2020 and are expected to dip by roughly 5% as we approach mid-2021, from where they are expected to climb again.

Concerning new deliveries, 1M SF of new space has already been delivered this year and there is 1.8M SF of office space currently under construction. Most of the 1.8M comes from build-to-suit construction for large users like Nike and Adidas, while speculative projects represent a small portion.