The Portland area industrial market entered 2020 with positive momentum from rent growth, absorption, new deliveries and growing demand from companies pivoting to a warehouse/delivery mindset. The initial shock of a pandemic induced shutdown slowed construction, tours and deal flow as all industries scrambled to adjust to business during Covid-19 in Spring of 2020.

By summer, Industrial tuned out to be the bright spot in the commercial real estate world as warehouse owners benefited from demand for direct-to-customer delivery. Industrial also received an unexpected boost from contractors and building materials companies that scrambled to meet the demand from homeowners remodeling, building decks and new housing starts.

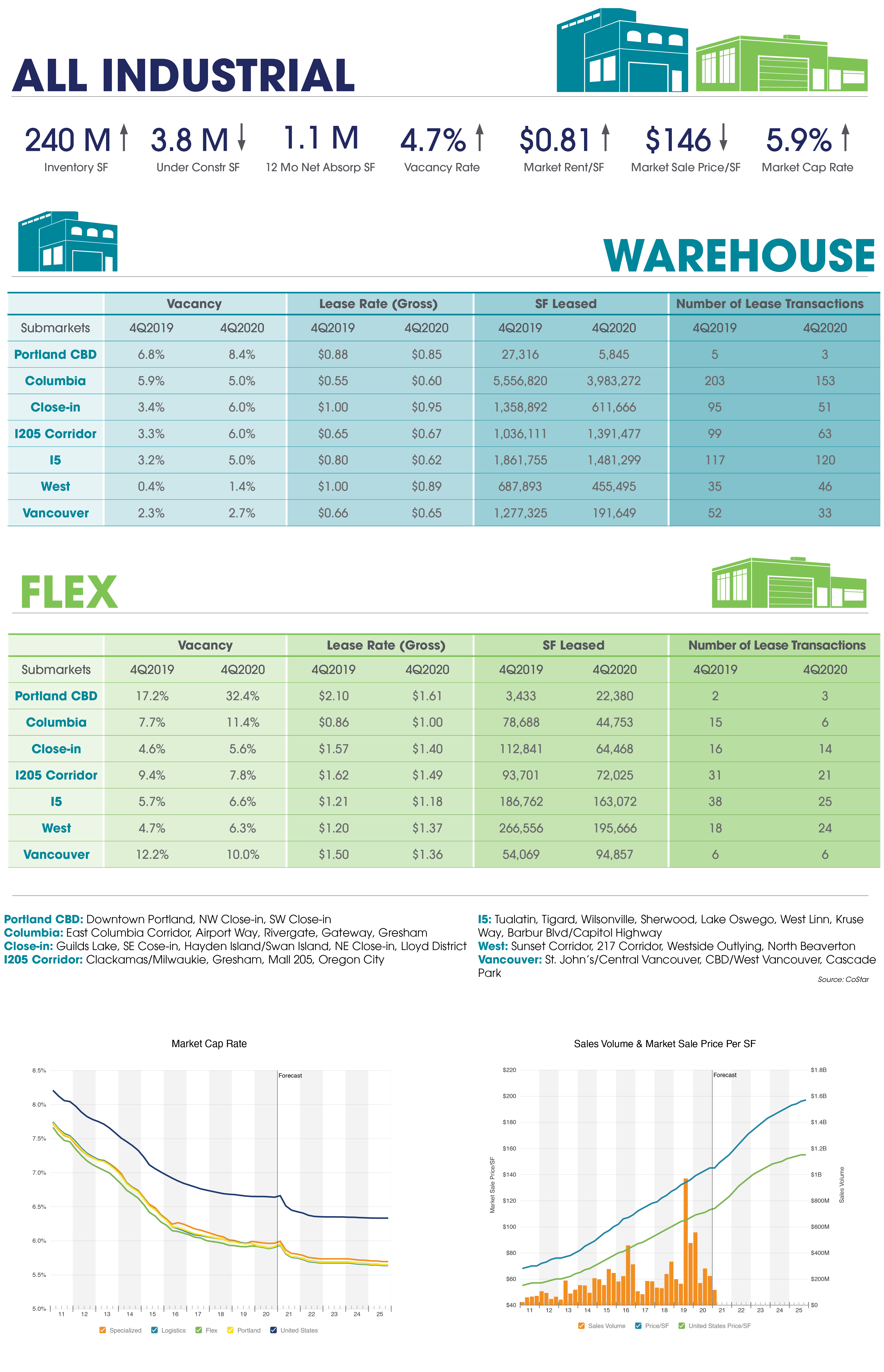

Portland’s overall vacancy rose to 4.7% at 4Q20 from 4.0% at the beginning of the year. Most submarkets followed suit, with the one exception being the Columbia Corridor which saw vacancy fall from 5.9% to 5% in 2020. With large spaces and institutional quality product, the Columbia Corridor is well positioned to serve the increased demand from national companies looking to establish warehouse to customer services.

Despite the market-wide vacancy increase, market rental rates gained slightly from $0.78/SF NNN to $0.81/SF NNN on a blended basis. Some of this rent growth can be attributed to contractual annual rent escalations in leases. But another factor is that the generation of warehouse spaces delivered and rented in 2020 was significantly more expensive to build than the year or two before. Those higher construction costs are passed along to the tenants through increased rent and the landlords’ leverage of having modern distribution space ready to lease.

After the very choppy 2020, Industrial real estate looks to return to steady positive metrics in 2021.